When a family member is a minor, legally incapacitated, or under amministrazione di sostegno (Italy's support administration regime), moving money from their bank account isn't a matter of signing a slip — it requires the green light of the giudice tutelare, the supervisory judge. The rule catches most people off guard the first time they encounter it, often right after being appointed guardian of an elderly parent or a child who has inherited money. But the logic is straightforward: protect the assets of those who cannot defend them on their own. Understanding how the procedure works, which acts need authorisation and which don't, and how to file a petition the judge will grant without back-and-forth, is the difference between a case closed in two weeks and months of follow-up requests.

What the law says: article 374 of the Italian Civil Code

The reference rule is article 374 of the Italian Civil Code, which lists the acts a guardian (tutore) cannot perform without authorisation from the giudice tutelare. Item 2 covers the collection of capital — a category the courts interpret broadly, and which includes the withdrawal of significant sums from bank accounts held by the protected person. The same article is referenced by article 411 c.c. for support administration and by article 394 c.c. for legal disability (inabilitazione), so it applies across all three protection regimes.

The logic is identical in each case: the guardian or administrator acts on behalf of someone who cannot directly oversee how their money is managed. The judge's authorisation is there to verify two things, and only two: that the withdrawal is necessary, and that it is proportionate to the stated purpose. It isn't a review of the beneficiary's lifestyle choices — it's a financial check.

What changed with the Cartabia reform

As of 28 February 2023, with the entry into force of legislative decree 149/2022 (the Cartabia reform of civil procedure), authorisations under article 374 c.c. now fall entirely within the competence of the giudice tutelare. Previously, the more significant authorisations went to the tribunal sitting as a collegial bench, with the giudice tutelare issuing only a non-binding opinion. Today the procedure is faster because it plays out before a single judge, in chambers, without formal hearings in most cases.

When authorisation is genuinely required (and when it isn't)

This is where we see most confusion. Not every movement on the protected person's account requires authorisation: it depends on the nature of the act and on what the appointment decree says.

For the guardianship of a minor or a legally incapacitated person, the general rule is this: ordinary administration acts (paying bills, buying everyday goods, collecting pensions or salaries) the guardian performs autonomously. Extraordinary administration acts — collecting capital, selling property, accepting inheritances, creating mortgages — require prior authorisation.

For support administration the picture is more nuanced. The appointment decree from the giudice tutelare spells out precisely what the administrator can do alone and what requires further authorisation. Decrees typically set a monthly withdrawal cap (for example 800 or 1,000 euros) within which the administrator operates freely for the beneficiary's day-to-day expenses. Above that cap, or for extraordinary operations, a specific petition is required.

One detail many discover only at the bank counter: the institution opens a vincolato account — an account constrained to the order of the giudice tutelare. Any operation above the set threshold requires the authorisation order to be produced. It isn't a formality — a bank that releases funds without authorisation is jointly liable with the guardian.

The most common cases requiring authorisation

In our experience, the petitions that reach the giudice tutelare most often concern:

- Withdrawals for extraordinary medical expenses (surgery, nursing homes, treatments not covered by the national health service)

- Purchase of a vehicle, especially when adapted for disability

- Collection of severance pay (TFR), life insurance policies, or insurance settlements

- Investing liquidity in low-risk instruments (Italian government bonds, conservative bond funds, life insurance policies) to counter inflationary erosion

- Renovation or accessibility work on the residential property

- Payment of the equitable indemnity due to the support administrator under article 379 of the Civil Code

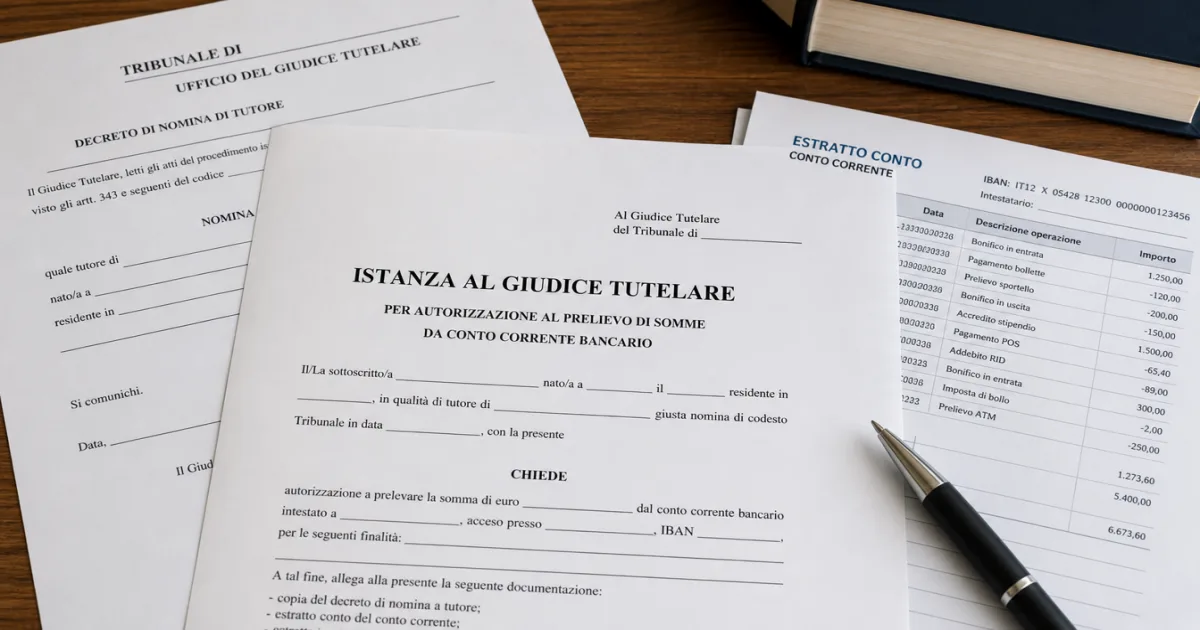

How to file the petition, step by step

The petition is filed with the Voluntary Jurisdiction registry of the competent tribunal — meaning the one for the protected person's place of residence, not the guardian's. The distinction matters when, for example, an adult child manages the affairs of a parent living in a different city.

The petition is on plain paper but must include:

- Full personal details of the guardian/administrator and the beneficiary

- Details of the appointment decree (case number, date, judge)

- The exact sum requested

- A precise, documented purpose for the expense

- Source and destination accounts for the funds

- The petitioner's signature

A 27-euro revenue stamp is attached to the petition, except in exempt cases. Proceedings involving minor children are exempt from the unified court contribution under article 10, paragraph 2, of presidential decree 115/2002. Copy fees remain payable to obtain the certified order to present at the bank.

Legal representation by a lawyer is optional. For simple, well-documented petitions many guardians proceed on their own, but when the amount is significant or the purpose complex — say, a financial investment — having a lawyer familiar with the specific tribunal's practice reduces the risk of rejections and integration requests.

The documents that make the difference

The most common mistake is filing a generic petition backed by a thin paper trail. The judge needs to come away with a clear picture: who the beneficiary is, what their financial situation looks like, why this specific sum is needed, and how it will be spent.

In our view, the documents that should never be missing:

| Document | What it's for | Practical notes |

|---|---|---|

| Guardian/administrator appointment decree | Establishing standing | Certified copy, not a plain photocopy |

| Petitioner's ID document | Identification | Must be in date |

| Recent account statement of the beneficiary | Confirming available funds | Last 3–6 months, no more than 30 days old |

| Quotes or pro-forma invoices | Justifying the amount | At least 2–3 quotes for expenses above €5,000 |

| Medical documentation | For healthcare expenses | Certificate from the treating or specialist doctor |

| Explanatory report | Setting out the context | 1–2 pages, dry and concrete |

The explanatory report is the document most often underestimated. It shouldn't be a rhetorical exercise: one page that explains who the beneficiary is, why the expense is needed now, and why the requested amount is proportionate. For readers who want to deepen their understanding of asset management best practices, our guide to safe investments in Italy can be useful, particularly when the petition concerns reinvesting the beneficiary's liquidity.

Real timelines and the urgency procedure

Timing depends on the tribunal. In medium and smaller tribunals, a well-documented petition is typically decided within 15 to 30 days. In the larger metropolitan tribunals (Rome, Milan, Naples) timing can stretch to 45–60 days during peak periods. The ruling is a decree, briefly reasoned as a rule, and communicated through the registry.

When documented urgency exists — a scheduled surgical procedure, a tax deadline, a time-sensitive purchase opportunity — the judge can be asked to rule under the urgency procedure. In these cases, where documents are in order, we've seen decrees issued in just a few days. The trick is to document the urgency with the same care given to the expense itself: a generic request for urgent treatment gets handled as an ordinary petition.

Once the decree is obtained, it must be presented to the bank together with the ID document. The bank then carries out the withdrawal or transfer as authorised. Keeping a copy of the decree and the transaction receipt is essential: both will be needed for the annual accounting report.

One operational detail that saves a return trip to the bank: ask the registry for two certified copies of the decree. One stays in the guardian's files, the other is handed to the bank. Some banks, when amounts exceed €25,000, trigger additional anti-money-laundering checks that can delay execution by another week — it pays to forward the documentation to the account manager in advance, so verifications run in parallel.

The mistakes that get petitions rejected

On this point it's worth being explicit. The recurring reasons for rejection or requests for additional documentation, in our observation:

Rounded-up amounts. Asking for €10,000 for a purchase that costs €7,300 is a move the judge spots immediately. The amount requested should match the documented expense, not a generous estimate.

Vague purposes. "For the beneficiary's needs" isn't a justification. The petition needs to specify what is being bought, from whom, and why. If it's renovation work, attach the cost breakdown. If it's treatment, attach the quote from the healthcare provider.

Outdated documentation. A six-month-old quote is considered stale. For healthcare and technical expenses, the working rule is to keep documents within 30 days.

Confusion between ordinary and extraordinary administration. Filing for authorisation on acts the appointment decree already covers is wasted time. Re-reading the decree carefully before drafting the petition is the first check to run.

Lack of transparency on the broader estate. If the beneficiary has multiple accounts, the full picture must be set out. The judge assesses proportionality against the entire patrimonial position.

What to do if the petition is rejected

A rejection isn't the final word. The petition can be re-filed addressing the judge's specific points, or an appeal can be lodged with the tribunal in collegial composition within 10 days of the decree being communicated, under article 739 of the Code of Civil Procedure.

In most cases, the first route is preferable: understand from the rejection decree what was missing (disproportionate amount, insufficient documentation, unconvincing purpose) and re-file with the integrations required. The collegial appeal is faster when the rejection turns on a debatable interpretation of the law, not when the issue is the quality of the documents.

For anyone new to managing a vulnerable person's assets, our analysis of current accounts best suited to specific needs is worth reading too, because the choice of bank and account type affects operational flexibility in the months following appointment.

The picture for those managing substantial assets

When the protected person's estate exceeds €50,000–€100,000, the approach shifts. The giudice tutelare assesses not only the individual operation but the overall management strategy: leaving large sums in a non-interest-bearing current account is, today, a choice that gets challenged at the annual accounting stage because of inflationary erosion.

In these cases it's worth presenting the judge with a management plan that includes investing part of the liquidity in low-risk instruments — Italian government bonds, conservative bond funds, Branch I life policies — and authorisation tends to come more easily when supported by an independent advisor's report attesting to the safety and convenience of the operation. Recent case law is clear: the judge doesn't block investments on principle, but wants to see rationality and prudence in the choices.

The guardian or support administrator should never lose sight of one point: every year a management accounting report must be filed. That's where patrimonial choices face their final review. A well-built petition, granted and then executed consistently with what was declared, is the best guarantee against surprises when the accounting is reviewed.

One last practical note on the annual report. Keeping every receipt, invoice, account statement, and copy of authorising decree in a single folder — physical or digital — turns the accounting moment from a nightmare into a half-day job. Anyone managing the affairs of an elderly relative over several years accumulates hundreds of transactions: without an archiving method, retracing the consistency between authorisations obtained and expenses actually incurred becomes a chore that can attract follow-up questions from the judge and, in the worst cases, challenges from other family members.

Managing the assets of a vulnerable person is a responsibility that weighs heavily, but it gets simpler once the logic of the system clicks: the giudice tutelare isn't an obstacle, it's a control that protects the manager as much as the managed. Prepare the documentation properly, be precise about purposes, and the procedure moves. When you're unsure about a specific act, an informal question at the registry before filing the petition is worth more than a thousand pages of pre-printed forms.