Opening a bank account online in Italy today takes less time than a coffee break: with SPID, the national digital identity, you can have a working IBAN in about fifteen minutes without setting foot in a branch. The process has changed a lot in recent years, but one step still trips up first-timers — proving who you are remotely. Here you'll find the real steps, the documents to keep within reach, the actual timelines, and the checks the bank is legally required to run, so you reach the signature without snags.

What You Actually Need Before You Start

The list is short, but it's worth getting it ready before you open the bank's site. You'll need a valid ID document (identity card, driving licence, or passport), your codice fiscale — the Italian tax code — or the health insurance card that carries it, a smartphone or a computer with a webcam, an email address, and a mobile number to receive OTP codes. Depending on the identification method you pick, you may also need a level-2 SPID or an IBAN already held in your name for the verification transfer.

On eligibility, no surprises: you must be of legal age and, for the vast majority of accounts, resident in Italy with an Italian codice fiscale. Non-residents have fewer options and almost always need a codice fiscale first; some digital banks and European neobanks are more flexible, but a primary Italian account generally assumes Italian residency. One detail that wastes a lot of people's time is photo quality — the document has to be legible, not expired, and shot without glare. A blurry or cropped photo sends the procedure back to square one.

Two cases deserve a warning. For a joint account, both holders have to identify themselves separately, each with their own document: the opening won't close until both checks are done. And if you're opening an account for a minor, you need the presence and consent of whoever holds parental responsibility, with the parent's document alongside the child's. In both situations, budget a few extra minutes over a single-holder account.

The Steps, From Start to Finish

Net of the differences between one bank and another, the sequence is always the same. You choose the bank and the plan (basic, premium, under-30). You fill in the form with your personal details, residence, and employment situation — that last one isn't the bank being nosy, it's an anti-money-laundering requirement. You upload front and back photos of your document. You identify yourself with one of the methods we'll cover in a moment. You sign the contract digitally, usually with an OTP code by SMS. At that point you receive the IBAN and the credentials to access the app.

The step that slows everyone down is identification. The others take a few minutes of form-filling; this is where it's decided whether you wrap up in a quarter of an hour or in two days.

Here's a practical example. Giulia, 28, an employee, wants a digital account to have her salary paid in and waive the monthly fee. She opens the bank's app at nine in the evening, fills in her details in five minutes, photographs her ID card, and chooses SPID for identification. She enters her credentials, confirms on the digital identity app, and signs the contract with the OTP that lands by SMS. By twenty past nine she has an active IBAN and a virtual card already loaded into Google Pay. The physical card will reach her within the week, but the account is effectively live straight away. Without SPID, the same path would have required a video call with an operator — doable, but on hours and waiting times far less convenient than nine in the evening.

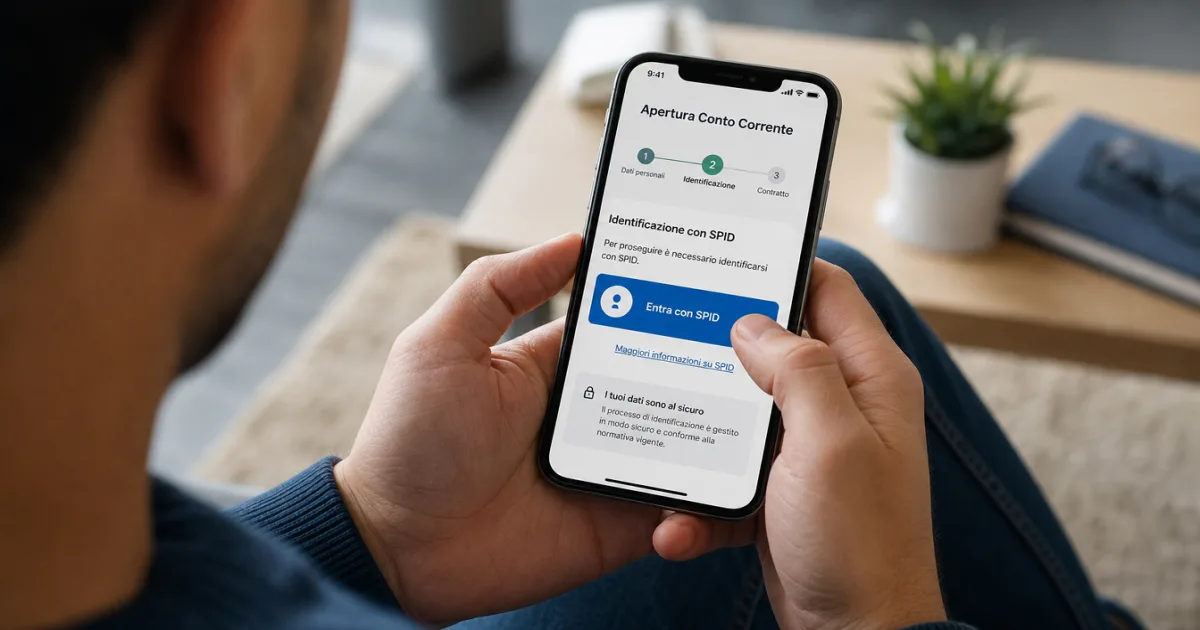

The Three Remote Identification Methods

The law requires the bank to establish with certainty who you are. To do that remotely, there are three routes, with very different timelines and requirements. SPID — and the CIE, the electronic identity card — is by far the fastest: the bank queries the public administration servers, confirms your identity in real time, and takes you straight to the signature. Video identification involves a short video selfie or a video call with an operator, where you frame your face and document; it often includes a "liveness" test (turn your head, read a code) to rule out photo fraud. The identification transfer, finally, means sending a small payment — even a single euro — from another account held in your name.

| Method | Time | What you need | Notes |

|---|---|---|---|

| SPID / CIE | A few minutes | Level-2 digital identity | The fastest; skips visual verification |

| Video selfie / video call | 5-20 minutes | Document + well-lit room, stable connection | May need a follow-up check by the operator |

| Identification transfer | 1-2 business days | An IBAN held solely in your name | The transfer must come from your own, non-joint account |

Which is best? If you have SPID, use it without a second thought: it's free, instant, and spares you both the video call and the wait for a transfer. If you don't have it and need the account quickly, video identification is the next best option — provided you have five minutes, a bright room, and a decent connection. The identification transfer still suits anyone who already holds another account and would rather not go on camera, but it's the slowest method and comes with a strict rule on ownership.

How Long It Takes: From Opening to a Working IBAN

With SPID, many banks make the account operational the same day, sometimes within minutes: Hype, SelfyConto, and ING let you get the IBAN and access the app in under a quarter of an hour. The virtual debit card is almost always available immediately in your phone's wallet, so you can pay by phone before the plastic ever arrives. The physical card comes by post within 3-7 business days.

With video identification the timeline stretches a little, because in some cases an operator has to confirm. With the identification transfer, count on one or two business days — the time it takes for the payment to register and clear. If you're in a hurry — say you need an incoming payment soon — SPID is the obvious call.

What It Costs to Open (and Keep) an Online Account

Opening an online account is free everywhere: no bank charges you for the procedure itself. The real cost is the monthly account fee, and here the range is wide. It runs from €0 with no conditions (BBVA, or isybank's base plan) to around €4 a month for accounts like Fineco or SelfyConto, almost always waived if you have your salary credited or are under 30.

The fee, though, isn't the whole story. The costs that really weigh sit elsewhere: stamp duty (imposta di bollo, €34.20 a year once your average balance tops €5,000), the commission on withdrawals at other banks' ATMs, and the credit card's annual fee, if any. On a digital account chosen with care, factoring everything in, your annual spend can stay under €30-€40. On the same profile, a traditional bank with no active promotions easily clears €150.

Put in numbers: on a digital account with the fee waived through salary credit and an average balance below €5,000, you can spend zero or close to it across a year — the only possible cost being a few euros in out-of-network withdrawals. Go above the balance threshold and you add the €34.20 of stamp duty, which is owed by law on any account anyway, digital or traditional. The point, in our view, is exactly this: the saving on an online account doesn't come from some trick, but from the absence of the fixed fee that, in a branch-based bank, funds the counters you — online — never use.

Anti-Money-Laundering Checks: Why the Bank Asks All This

When you're asked what you do for a living, where your money comes from, or whether you hold public office, it isn't intrusiveness: it's customer due diligence, required under Legislative Decree 231/2007, Italy's anti-money-laundering law. It applies identically to an account opened in a branch and one opened from your sofa. The Bank of Italy confirms it: online accounts are subject to the same regulatory obligations as traditional ones, anti-money-laundering controls included.

That brings us to a point many people overlook out of unease. An Italian digital bank is a fully licensed bank, supervised exactly like the others — we explain this in detail in our piece on the functions of the Bank of Italy. Your deposits are protected by the Interbank Deposit Protection Fund (FITD) up to €100,000 per holder, identical to what happens at the counter. Opening online doesn't mean exposing yourself more — it just means signing digitally instead of on paper.

In the vast majority of cases the questions stop at occupation and the account's purpose. Deeper checks kick in only in specific situations: if you hold or have held a prominent public role (a politically exposed person, in the jargon), if the expected activity is far higher than your declared profile, or if the funds arrive from abroad. It isn't suspicion aimed at you — the bank faces heavy penalties if it skips these steps, which is why it insists. Answering candidly is in your interest too, because it avoids account freezes after verification.

Mistakes to Avoid When Opening an Online Account

A mistake we see often involves the identification transfer itself: people who try it from an account held jointly with a partner find the verification blocked, because the law requires the payment to come from an account held by the applicant alone. Same scene with video identification done in a dimly lit room or with the connection dropping halfway — the operator can't confirm the data and you have to start over.

Then there's the opposite mistake, subtler. Opening accounts in rapid succession to chase promotions, without closing the old ones, exposes you to double stamp duty and forgotten fees that switch on after the first free year. Before signing, it's always worth reading the current product information sheet (foglio informativo) and working out whether the account fits how you actually use money — to think that through, we've compared traditional and digital banks. One last rule, non-negotiable: during the opening, no bank will ever ask you for a PIN, password, or codes by email or phone. If that happens, it's a scam.

What to Do Right After Opening

As soon as the account is live, it pays to sort out three things. Add the virtual card to your phone's wallet so you can start paying right away. Set your withdrawal and spending limits to match your real habits. Turn on push notifications for every transaction — it's the simplest way to catch something wrong the instant it happens.

If this account replaces your main one, use the portability rules. Under the payment-account switching service, the new bank automatically moves recurring transfers, utility direct debits, and the balance from the old account within 12 business days, as set out in the framework supervised by the Bank of Italy. You don't have to chase anyone. Finally, remember to give your new IBAN to your employer: a salary credit is almost always the condition that waives the fee.

One note on the cash you keep parked. Many digital banks pair the current account with a savings account that pays interest on unrestricted balances: if you've got a cushion you don't touch for months, it's worth activating rather than leaving it earning nothing on the current account. Be careful, though, not to let the average balance on the current account climb above €5,000 without reason, since that's the threshold that triggers the annual stamp duty.

On the old account, finally, a common-sense rule: don't close it the same day. Leave it open for a month or two, with a few euros in it, until you're sure every recurring debit has migrated. Only when you see your salary and direct debits landing on the new IBAN should you request closure of the old one — free by law — without risking a missed payment on a utility or instalment.

The practical advice is just one line: pick an account with a waivable fee, open it with SPID to avoid the wait, and actually use it for a couple of months before closing the old one. If something doesn't convince you, switching costs nothing — and these days the new bank handles the move for you.

This article describes the Italian process for opening a bank account and the relevant Italian regulations. Information is provided for educational purposes and does not constitute financial, tax, or legal advice. Rules and figures refer to the Italian regulatory framework as of the publication date and may change.