If you hold even €50 of Bitcoin on an exchange, Italian tax law gives you a reporting obligation. The rule that used to exempt small amounts is gone, and as of 2026 the rates have changed again. Here is what you actually have to report, which section of the 730 form or income tax return to use, how much you pay, and how to calculate your gain without slipping up — including the distinction, often missed, between what you declare this year and what you will pay on the trades you make right now.

When You Must Report Crypto (and When You Don't)

Start from the point that causes the most confusion: holding cryptocurrency and selling it at a profit are two different things, and they trigger separate obligations. Simply holding crypto activates the monitoring requirement — you have to report your crypto-assets in your tax return even if you sold nothing during the year and earned nothing. This applies from the very first euro, with no minimum threshold, for crypto held on foreign exchanges (Binance, Coinbase, Kraken), in self-custody wallets (Ledger, Trezor, MetaMask), and on Italian exchanges under the declarative regime.

Take the most common case. You bought Bitcoin two years ago, it has appreciated, but you never sold. You owe no tax on the gain — because you haven't realized it — but you are still required to list that crypto in the monitoring section and to pay the holdings tax discussed further down. Holding and nothing more costs you no income tax, but it does not exempt you from reporting.

Actual taxation kicks in only when you realize income. Here Italian law — introduced by the 2023 Budget Law through Article 67, paragraph 1, letter c-sexies of the TUIR (Italy's consolidated income tax act) — draws a precise line between taxable and neutral operations.

Operations That Trigger Taxation

A taxable capital gain (or loss) arises when you sell crypto for euros or another fiat currency, when you pay for goods or services in cryptocurrency, when you convert a volatile crypto into a stablecoin, and when you swap one crypto-asset for another of a different nature. That last point is subtle: according to circular 30/E of the Italian Revenue Agency (Agenzia delle Entrate), swapping Bitcoin for a dollar-pegged stablecoin is a disposal in full, because the two assets serve different economic functions. The same logic applies, from 2026, to many conversions that used to be handled loosely.

Neutral Operations You Don't Pay On

Transfers between wallets you own are not taxable events — moving Bitcoin from an exchange to your own Ledger is not a sale — and neither is a swap between crypto-assets with the same characteristics and functions. The classic example is exchanging Bitcoin for Ethereum: the Revenue Agency treats both as "virtual currencies" with an equivalent function, so the operation is neutral and the euro cost basis simply carries over to the new crypto. Careful, though: neutral does not mean invisible. You still have to track costs, dates, and the exchange rate applied, because that figure is what you will use to calculate the gain when you eventually cash out into euros.

The Two Sections to Fill In: Monitoring and Capital Gains

One of the more useful recent changes is that people who file with the simplified 730 form (Italy's return for employees and pensioners) can now handle crypto directly, without being forced onto the standard Redditi PF return. The sections change name but do the same job across the two models.

| What you report | 730 form | Redditi PF return |

|---|---|---|

| Crypto holdings (monitoring) | Section W | Section RW |

| Realized capital gains | Section T | Section RT |

| Tax on crypto holdings | Section W, part II | Section RW, part II |

| Staking, airdrop, mining income | Section T / L | Section RT / RL |

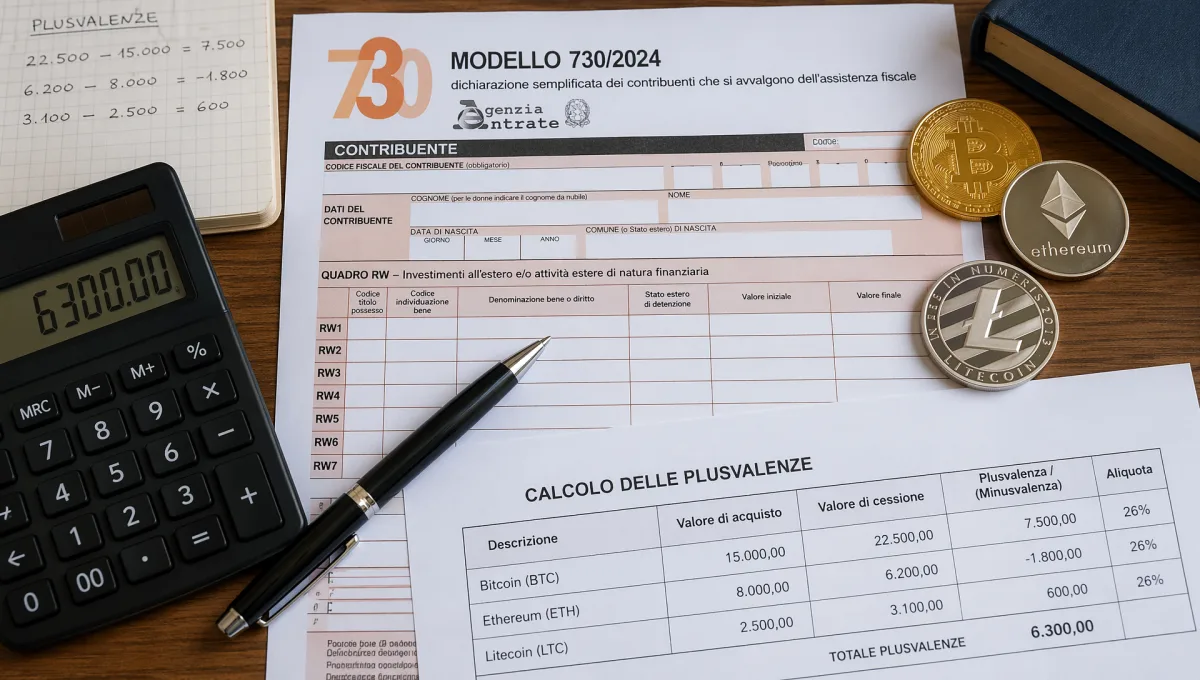

In the monitoring section (RW or W) crypto is reported under asset code 21, showing the value at the start and end of the year. You always fill it in, even for mere holding. The capital-gains section (RT or T), by contrast, you complete only if you carried out taxable operations: if all you did during the year was buy and hold, this section stays empty.

How Much You Pay: 26% for 2025, 33% from 2026

This is the part almost nobody explains correctly, and it is worth reading twice. The flat substitute tax on crypto capital gains depends on the year in which you realized the gain, not the year in which you file.

For gains realized in 2025 — the ones you declare now, in the 730/2026 or the Redditi PF 2026 return — the rate is still 26%. For operations realized from January 1, 2026, the rate rises to 33%, under the 2025 Budget Law confirmed by the 2026 one; you will only see that higher charge in the return you file in 2027. In practice, the form you are filling in these months still pictures a 26% world, while the sales you make today already run at 33%.

There is one meaningful exception. E-money tokens denominated in euros and compliant with the EU's MiCA regulation — essentially certain euro stablecoins — stay taxed at 26% even after 2026. It's a legislative choice that favors instruments closer to electronic money over speculative trading, and it creates a bit of asymmetry for anyone holding spot Bitcoin. For where the different coins and stablecoins sit in this picture, see our analysis of the top cryptocurrencies of 2026.

A concrete example makes it clearer. You bought 0.5 Bitcoin for €20,000 total and sell at €32,000. The gain is €12,000. If the sale happened in 2025, you pay 26%: €3,120. If you make the exact same trade in 2026, you pay 33%: €3,960. That's €840 of difference on an identical gain, purely because of the date.

How to Calculate the Capital Gain, Without Surprises

The gain is the difference between the proceeds received (or the normal value, in the case of a swap) and the documented purchase cost. The key word is documented: if you can't prove what you paid for the crypto you're selling, the tax office assumes a cost of zero and taxes the entire amount received. On a €10,000 cash-out with no documentation, that means paying tax on all €10,000, not on the real profit. Keeping the transaction history from every exchange and wallet isn't a formality — it's what separates a correct tax bill from an unjustified one.

When you bought the same cryptocurrency at different times and prices, the LIFO method (Last In, First Out) decides which "lot" you're selling: the most recently purchased quantity is treated as sold first. It's the same criterion used for other financial instruments, and it has to be applied consistently across the whole year.

One detail trips up many people: currency. If you sell crypto and the proceeds land in dollars rather than euros, the amount is converted at the exchange rate on the day of the operation under Article 9 of the TUIR, using Bank of Italy reference rates. The same principle applies to a swap into a crypto of a different nature, where you take the normal value of the asset received at the moment of the exchange. Noting the rate, source, and time for each operation isn't pedantry: in an audit, the traceability of the rate is often the deciding factor.

And NFTs? They fall under the same rules when they have a liquid market and a value quantifiable in money — an NFT from a regularly traded collection is treated like any other crypto-asset. For unique pieces with no reference market, held as digital art for personal collection, the assessment is case by case: when in doubt, reporting is the prudent choice.

Losses shouldn't be thrown away. Since 2024, crypto losses offset only gains on crypto-assets: you can no longer use them to reduce profits on stocks or ETFs. Any unused excess carries forward against gains in the four following tax years, provided you reported it in the return for the year you realized it. Forget to declare it, and you genuinely lose that loss.

The Annual Tax on Crypto Holdings (the Former Stamp Duty)

Beyond the tax on gains, there's a small wealth levy that many discover only afterward: the tax on the value of crypto-assets, heir to the stamp duty. It applies at 0.2% per year on the euro value of your crypto as of December 31. If your holdings were worth €15,000 at year-end, the tax is €30. When the crypto sits with an Italian intermediary that already applies stamp duty, you do nothing; when it's on foreign exchanges or in self-custody, you settle the tax yourself in the return, in part II of the RW or W section.

Staking, Airdrops, and Mining: The Income People Forget

Anyone who only buys and sells tends to overlook income earned in other ways — the tax office does not. Staking rewards, interest from decentralized-finance lending protocols, and tokens received through airdrops count as miscellaneous income and are taxed on their euro market value at the moment you receive them. The same goes for occasional mining. If you later sell those tokens at a profit, a second layer of tax applies to the gain accrued from that point onward.

A separate matter for anyone mining or staking on a continuous, organized basis: that's no longer miscellaneous income but business activity, with a VAT number (partita IVA) and an entirely different set of rules. The line between hobby and professional activity is where much of the fiscal risk lies for those operating at meaningful volume.

Declarative vs Managed Regime: Who Does the Math for You

Until recently, crypto investors had a single path: calculate everything themselves and report it. That's the declarative regime (regime dichiarativo), the only one available to those operating on foreign exchanges or in self-custody. It works, but it puts every responsibility on you: aggregating transactions across all wallets, applying LIFO, handling exchange rates, carrying losses forward. For someone trading a few times a year it's manageable; for active traders it becomes a job, often outsourced to specialized software or an accountant.

The new development is that some Italian intermediaries are starting to offer the managed regime (regime amministrato), on the back of Revenue Agency guidance (ruling 135/2025). Here the exchange acts as a withholding agent: it calculates gains using LIFO, withholds the substitute tax at the moment of disposal, pays it via the F24 form (Italy's unified tax payment slip), and manages the carry-forward of losses. The practical upside is that you don't fill in the RT section and don't worry about payment deadlines. The downside is that it works only for crypto held with that intermediary: move the assets to an external wallet or use several platforms, and you're back, fully or partly, in the declarative regime. In our view it's an appealing option for anyone who wants simplicity and keeps the bulk of their holdings on a single Italian operator, and less so for those used to moving between exchanges.

Step-Up, Penalties, and What Changes from 2026

In recent years lawmakers have repeatedly opened windows for a value step-up (rivalutazione, or affrancamento): by paying a substitute tax — the latest edition was 18% on the value as of January 1, 2025 — you could reset the fiscal value of your crypto, shrinking future gains. That window closed at the end of 2025, but it's a tool the legislator tends to reintroduce: if you expect large gains ahead, it's worth watching the next budget laws.

On penalties, failing to complete the RW section costs from 3% to 15% of the undeclared value (doubled for non-cooperative countries), while an omitted income return carries far heavier sanctions. The good news: until an audit arrives, you can fix your position voluntarily through the voluntary disclosure mechanism (ravvedimento operoso), which sharply reduces the penalties. If you have undeclared prior years, regularizing before the Revenue Agency notices is almost always the cheaper route — not least because the net is tightening.

From 2026, crypto enters the calculation of the ISEE (Italy's household means-test indicator): a family's crypto wealth now weighs on the metric used for benefits and subsidized services. And from 2027 the EU's DAC8 directive becomes operational, requiring exchanges across the Union to report client data automatically to the tax authorities. The era when crypto slipped under the radar is over: traceability is now the rule. To place crypto taxation within the wider Italian tax system, our guide to taxes in Italy is a useful companion; and if you want to understand where crypto fits in a broader portfolio, read our investment strategies for 2026.

The dates to mark: the 730 form is due by September 30, the Redditi PF return by October 31. For the operational detail and the codes for each section, the official reference remains the Italian Revenue Agency, with up-to-date forms and instructions.

The practical advice is just one thing: don't wait until spring to get organized. Download today the transaction histories from every platform you use and keep them in one folder, even just a spreadsheet. When you open the return, the difference between half an hour of work and a week of panic comes down to exactly that.

This article describes Italian regulations and financial products. Information is provided for educational purposes and does not constitute financial, tax, or legal advice. Rules and figures refer to the Italian regulatory framework as of the publication date and may change.